Fixing the Rigged System

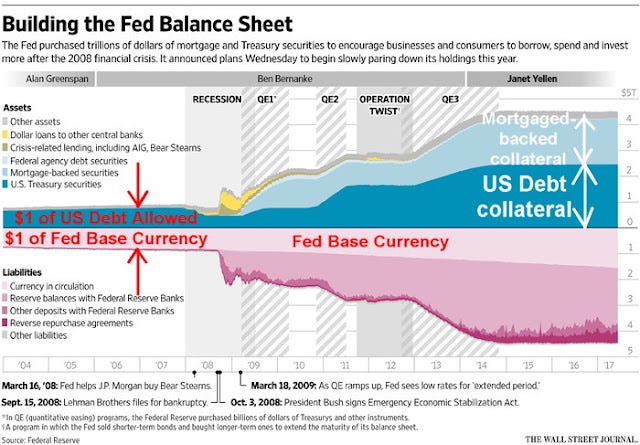

Over the past several weeks, I’ve shown you how it is that as long as the Federal Reserve private banking system controls the issuance of America’s money supply, it will remain mathematically impossible to pay off the national debt or sustain a balanced federal budget. For one thing, we know that is true because before the Fed can place new base dollars into circulation, U.S. sovereign debt of equal dollar value must be received by the Fed and held as collateral. One dollar of U.S. debt allows the Fed to create one dollar of base currency.

Furthermore, at the member bank level, such as that of Wall Street banks, the American money supply is created and loaned into circulation, at interest. And because Wall Street does not issue dollars to pay the interest, the only way to pay it is for the people to keep borrowing more dollars…from Wall Street.

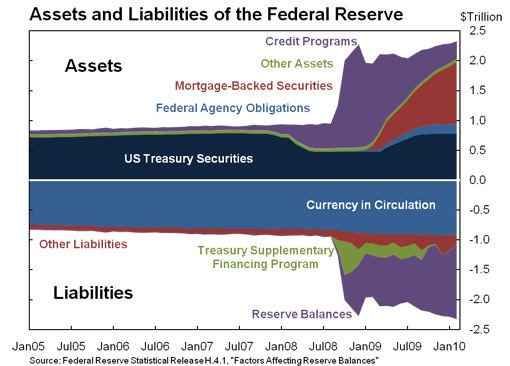

And so, if you look back at the Fed’s balance sheet leading to the financial crisis of ’08 and ’09, you would see an orderly balance between base currency the Fed had issued on one side, and an equal dollar value of collateralized U.S. debt on the other, just as I indicated. For each dollar of base currency in circulation, there was an equal balancing dollar of U.S. debt to secure it. That’s one reason they call U.S. debt instruments, “securities.” Under the Federal Reserve system, U.S. debt is necessary to secure the issuance of new base currency. What that really means is that, ultimately, the American people are on the hook to pay it back.

It Takes $1 of US Debt to Serve as Collateral for $1 of Fed Base Currency

But as we spoke last week, since the financial crisis a decade ago the Fed’s balance sheet has become a jumbled mess, the sight of which ought to convince any sane economist that the underlying problems causing the crisis a decade ago still persist. Those problems have merely been masked by more and more money printing and Fed manipulation, requiring of course more and more U.S. debt to secure each newly-issued base dollar, leaving the state of affairs I describe.

History of Fed Balance Sheet Since Collapse of '08 and '09

To keep the system liquid and profitable for Wall Street, after the crisis the Fed programmed the purchase of enormous amounts of bad debts from its banks, and still holds those questionably-performing “mortgage-backed securities” on its balance sheet. The Fed also purchased enormous amounts of U.S. debt, which it recently attempted to sell off. That is why interest rates climbed last year, why the stock market halted its meteoric ascension, and why Trump stepped in to stop what he refers as, “balance sheet tightening.” The Fed is stuck because it cannot get rid of its bad debt. And if it “fire sales” the U.S. debt it holds, the money supply would contract and interest rates would rise, intensifying the problems the dying system is already experiencing.

Recall from the last couple of weeks I showed you how once the Fed issues new base dollars and deposits them into an account of one of its member banks, such as Goldman Sachs, the rules allow Goldman to effectively multiply that those dollars up to a factor of nine, loan out the result or invest it by purchasing stocks listed on various stock exchanges. The dynamic I just described is how the Federal Reserve System builds and maintains market bubbles and manipulates stock and commodity prices.

The situation I describe is nothing President Trump caused, but is instead one he inherited from the previous two administrations after 100 years of Federal Reserve operation. This is how a debt-based economy always ends up, unsustainable debt. Trump is tasked to fix the problem, which he has already begun. But until he formally activates that process, Trump will avoid speaking meaningfully on the subject of rising U.S. debt or balancing the budget, his primary concern of course to avoid abruptly influencing domestic and world markets depending on the dollar for stable trade.

So how do we know Trump plans to fix the system? Trump has said it over and over, “the system is rigged.” Indeed, it is. Why would Trump tell the American people and the world that this system is “rigged,” unless he plans to fix it? He wouldn’t. Why would Trump continually point out the dishonest media charged with helping to perpetuate a system rigged every way imaginable unless it was? Again, he wouldn’t. When one understands the circumstances of Trump’s constant, sharp and unprecedented criticisms of the Fed’s handling of the economy, Trump knowing that the system cannot be fixed from within, it is a short putt that he plans to deal rationally with the Fed as one of his most pressing initiatives in a second term. Trump knows the U.S. debt problem cannot be remedied as long as the Fed controls the currency.

And for some folks who continue to believe that President Trump is part of the establishment he fights against for their interests, why would he seek to overhaul a system that he, himself, might depend upon in maintaining his own status among the rest? Again, he wouldn’t.

The bottom line is that to ever have a chance to fix this broken system, to balance our federal budget, or to pay off the national debt and return power to the American people depends on two things, re-electing President Trump for a second term and electing members of Congress who understand the problem and pledge to support Trump’s efforts to dismantle and replace the broken and dying Federal Reserve.